Currency depreciation, oil shocks threaten to deepen the pressure

Infographics: TBS

“>

Infographics: TBS

Savers in Bangladesh saw the real value of their bank deposits decline in 2025 as inflation outpaced interest rates, effectively eroding purchasing power despite continued growth in deposits across the banking system.

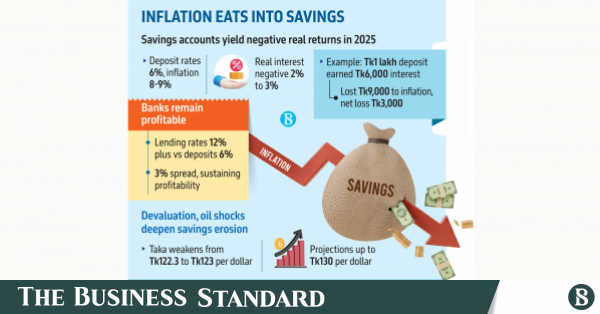

After adjusting for inflation, the real interest rate on deposits remained negative by 2% to 3%, meaning depositors are losing value on the money they stashed in bank accounts.

Bangladesh Bank data show the weighted average interest rate on overall deposits was around 6% in 2025, when average inflation was between 8% and 9% for most of the year, according to the central bank’s report titled “Banking Sector Update 2025”.

This means that savers earned less on their deposits than the rise in their living costs.

A depositor holding Tk1 lakh in a bank account would have earned around Tk6,000 in interest over the year, while inflation eroded roughly Tk9,000 in purchasing power, leaving the saver about Tk3,000 worse off in real terms.

Banks, however, have largely maintained profitability. With lending rates above 12%, banks retained a spread of more than 3% – the difference between lending and deposit rates – even after accounting for operational and provisioning costs.

Speaking to The Business Standard, Ezazul Islam, director general of the Bangladesh Institute of Bank Management (BIBM), said although the real interest rate appeared negative when considering the weighted average across overall deposits, returns on term deposits of one year and above remained slightly positive.

However, he warned that devaluation would further deepen the negative return and erode the purchasing power of savers, meaning that keeping money in banks may no longer be profitable.

Devaluation, oil shocks to deepen erosion

Pressure on deposit returns is feared to intensify if the central bank moves towards gradual currency depreciation to protect foreign exchange reserves amid rising energy import bills triggered by the ongoing Middle East conflict.

A fall in the taka will deepen losses for savers, as devaluation increases the cost of imported goods and leads to a rise in headline inflation, turning the real interest rate even more negative and further reducing savers’ purchasing power.

The exchange rate has already begun to depreciate gradually since 8 March, as the dollar rose close to Tk123 after remaining stable at Tk122.30 for months. The exchange rate band prepared daily by the central bank, based on currency movements of trading partners, suggests the dollar could reach Tk130.

At the same time, latest increase in oil prices have already started affecting domestic markets, raising production and transportation costs and pushing up the prices of almost everything.

Supply disruptions have also affected key raw materials used by many industries due to the closure of major sea routes between the Gulf and Asian markets. Entrepreneurs in export and domestic industries have indicated that import costs for some raw materials and chemicals have surged between 10% and 183%.

The combined shock from higher oil prices and currency depreciation is likely to fuel inflation further, eroding the purchasing power of savers.

Savers have little option

Despite negative returns, bank deposits continue to grow due to the lack of alternative investment options amid economic uncertainty, BIBM DG Ezazul said.

For many individuals and families, the choice remains limited. Land prices are beyond reach, instruments such as secondary bonds or provident funds are not open to the public, and informal schemes carry significant risks.

The capital market is highly volatile, making it difficult to invest in the current situation, which forces savers to deposit money in banks, he said.

In this situation, the central bank should maintain its high policy rate to safeguard depositors, he added.

Despite negative growth in real income, banks are receiving more deposits, which bankers say reflects people’s trust in the traditional banking system. The rate on fresh deposits turned positive from June 2025 onwards, according to the central bank report.

“Despite these low or near-zero real returns, overall deposit growth continued to rise, suggesting that savers prioritised financial safety, accessibility, and remittance-related inflows over purely return-driven motivations,” the report said.

“This resilience in deposit behaviour indicates strong confidence in the formal banking system even amid limited real gains,” it said, attributing the persistence of deposit growth amid negative real returns to the public’s enduring confidence in the formal banking system.

This contrasts with the suffering of depositors, particularly those with more than Tk2 lakh, in some troubled banks that have been unable to return their money.

Small and middle tiers lead the deposit growth

Bank deposits grew by more than 11% to Tk21 lakh crore by December 2025, from Tk18.8 lakh crore a year earlier, largely propelled by higher inflows of remittances.

Much of last year’s deposit growth came from small and middle-tier accounts. Accounts with balances up to Tk2 lakh – representing about 13% of total accounts – and those up to Tk25 lakh – about 55% – both showing significant increases from the previous year.

Deposits in the latter category rose to Tk6.52 lakh crore last year from Tk5.52 lakh crore in the previous year, suggesting that middle-income households continue to rely on banks as their primary savings vehicle.

Conversely, the number of very large accounts above Tk25 crore declined, suggesting a redistribution of deposits towards smaller holders and greater diversification of the overall deposit base.

These trends highlight that Bangladesh’s deposit structure is increasingly driven by retail and middle-tier savers, reflecting the expansion of inclusive and digital banking initiatives while emphasising the need for sustained depositor confidence and prudent interest rate management, the central bank report said.

Savers lose, banks gains

Although savers have been losing the value of their money, banks have remained profitable as high lending rates have kept spreads elevated.

When deposit rates averaged slightly above 6%, lending rates were more than 12%, exceeding the inflation rate during the year, according to data from Bangladesh Bank.

Explaining the reason behind the high lending rate, SM Mainul Kabir of SBAC Bank said borrowers could not enjoy the benefit of low deposit rates due to high default loans.

He said banks can lend up to Tk87 out of deposits of Tk100. Out of that Tk87, non-performing assets account for Tk10 to Tk15, allowing banks to lend a maximum of Tk75.

“If banks lend at 12%, they earn Tk12 annually, while operational and deposit costs exceed Tk10,” he said.

He added that banks would face operational losses if there were no additional income from charges and fees.

Despite relatively low deposit rates, high default loans have increased financing costs and squeezed private sector lending, he said.

The central bank report shows that the advance-deposit ratio (ADR), which measures how much of deposits are used for lending, declined to 85.8% in 2025 from 89.3% in December 2024, indicating a shift towards liquidity accumulation amid tightening regulatory requirements and heightened credit risk.

Total loans grew by only 5.6% during the year, while foreign banks recorded negative growth of 11.3%.

Islamic banks continued to show overexposure, with ADRs close to 120%, raising concerns about potential liquidity stress and over-lending tendencies. Similarly, several fourth-generation banks maintained ADRs above 100%, reflecting aggressive credit expansion strategies aimed at rapid portfolio growth.

In contrast, foreign banks adopted a more cautious approach, keeping their ADRs relatively low and maintaining adequate liquidity buffers and risk resilience.

Overall, the declining ADR across the banking system signals improving liquidity buffers, possibly at the cost of slowing credit growth, according to the central bank report.