The Federal Reserve’s board of governors

Kevin M. Warsh takes the reins of the Federal Reserve at a critical juncture for the economy, and for the central bank itself.

As Fed chair, a role he will soon assume, Mr. Warsh will need to navigate a delicate economic moment, a president who demands lower interest rates and an increasingly divided leadership committee — one whose members will now include Jerome H. Powell, the departing Fed chair.

An unusual transition

For the first time since 1948, a former Fed chair will remain with the central bank past the end of his term. Mr. Powell’s decision to stay as a board governor reflects his concerns over the Fed’s independence amid demands from the Trump administration for lower interest rates.

The Justice Department investigated Mr. Powell and the Fed over renovations to its headquarters, a move that was largely viewed as a pretense to exert pressure. Last month, the department dropped the inquiry but said it could reopen it at any point.

President Trump is also trying to oust Lisa D. Cook, a Biden-appointed governor. Whether he has standing to do so is now before the Supreme Court.

Mr. Powell’s continued presence means that Mr. Trump might not have an opportunity to nominate another governor to the seven-member board until January 2028, when Mr. Powell’s term as governor expires.

Trump appointees could be a majority of the Fed board by the time he leaves office

Interest rate pressures

A key question for Mr. Warsh as his tenure as chair begins is whether he will do Mr. Trump’s bidding as the president’s nominee — something that Mr. Warsh has repeatedly denied.

Mr. Trump has expressed a desire for rates to fall to 1 percent or even lower to stimulate economic growth. At its April meeting, the Fed kept the federal funds rate, its benchmark interest rate, at a range of 3.5 to 3.75 percent.

The Fed uses its benchmark interest rate to steer the economy with two main goals in mind: to keep inflation levels low and the labor market stable and healthy.

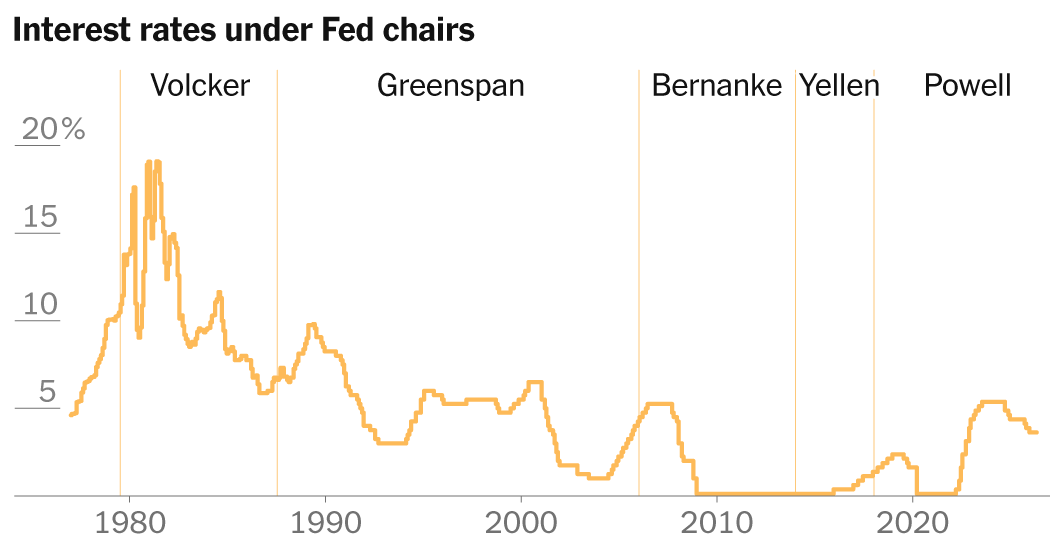

During a period of runaway inflation in the 1980s, the chair at the time, Paul Volcker, pushed the Fed to ramp up interest ratesto double digits to slow down price increases. The efforts worked, but at the cost of two recessions.

The benchmark interest rate under recent Fed chairs

Mr. Powell, who also faced inflation challenges as chair, often referenced the Volcker era. During the Covid recovery period, inflation rose to its highest level in decades. After mistakenly arguing at first that higher prices were likely to be “transitory” and that raising interest rates wasn’t necessary, Mr. Powell and his colleagues were forced to change course. They raised interest rates from near-zero in 2022 to as high as 5.5 percent by July 2023.

Economic conditions during Powell’s term as chair

Since the onset of the Iran war, rising energy prices have pushed prices up yet again, and some Fed officials believe that lowering rates will lead to a resurgence of inflation. At the same time, the labor market has remained relatively solid, further weakening the case for cuts as a way to lower borrowing costs and stimulate growth.

If the Volcker era was a guide for Mr. Powell, Mr. Warsh might be looking for parallels to another point in Fed history — the personal computing revolution of the 1990s.

Alan Greenspan, then the Fed chair, resisted the call to raise rates during a time when many feared the economy was running too hot. He argued that the United States was experiencing a productivity boom, meaning that strong growth was unlikely to be coupled with inflation, a hunch that turned out to be correct.

Mr. Warsh has said he believes the country is on the verge of a similar productivity boom today, ushered in by artificial intelligence. If that turns out to be the case, it could clear a path for the Fed to cut rates without stoking inflation.

A $6.7 trillion balance sheet

Interest rates are the most visible aspects of the Fed’s efforts to steer the economy. But the central bank also plays another pivotal role, as an investor.

It regularly buys government bonds, mortgage-backed securities and other assets. These assets are balanced by the Fed’s so-called liabilities, or debt that it owes to others. Those include primarily the paper currency that moves in and out of circulation and the deposits it holds for banks, also called “reserves.”

In times of economic stress, the Fed often supercharges its investments. At the height of the 2008 financial crisis, it bought enormous quantities of Treasuries and mortgage-backed securities to help bring down long-term interest rates — part of a policy known as “quantitative easing” intended to keep borrowing across the economy affordable.

Federal Reserve assets and liabilities as a share of G.D.P.

Mr. Warsh, who was then a Fed governor, was initially supportive of the effort. But he soured on the policy, arguing that the Fed was distorting financial markets. He resigned in protest in 2011.

The central bank’s balance sheet has since ballooned as a result of another wave of quantitative easing, during the pandemic.

Reducing the more than $6 trillion of assets on the Fed’s balance sheet is now a priority for Mr. Warsh. But there are internal disagreements over whether or how to do it.

A new era of internal divisions

During his confirmation hearing about how he would run the Fed, Mr. Warsh said that he favored “messier meetings” and a “good family fight.”

He might soon be getting his wish. Decades of little to no formal disagreement among the Fed’s top officials came to an end during the Powell era.

A rate decision requires agreement from a majority of the 12 voting members on the Fed’s rate-setting committee, which consists of all seven board governors, and a rotating set of five presidents of the Federal Reserve’s regional banks. Presidents have historically broken ranks more often than governors, whose objections have been rare. Mr. Powell’s tenure featured dissents by both, and in opposite directions.

Recent Fed dissents over rates

At Mr. Powell’s final meeting as chair in April there were four dissents, the most since 1992, when the Fed decided to leave rates unchanged. Three regional presidents supported the decision to hold rates steady but wanted the Fed to signal that the next move was not necessarily a cut. (Stephen I. Miran, the departing Trump-appointed governor, voted in favor of a rate cut.)

Such public disagreement among Fed officials, especially governors, could stoke fears that the central bank lacks conviction in its monetary policy decisions.

Mr. Powell’s decision to remain on the board is another wild card. He has said he has no intention of undercutting Mr. Warsh’s authority, but his presence alone will undoubtedly carry much weight at the Fed, and his vote could even be a tie-breaker if dissent within its ranks persists.