Highlights

- Tehran reportedly closes Strait of Hormuz

- Hormuz is crucial for global oil and LNG trade

- It handles 20% of oil and 20% of LNG shipments

- Bangladesh’s 18 of 22 LNG cargoes for March-May scheduled via Hormuz

- Prolonged closure may force Bangladesh to buy costly spot market LNG

- Fertiliser imports unaffected as no active Middle East procurement pending

- Current fertiliser stock sufficient until November

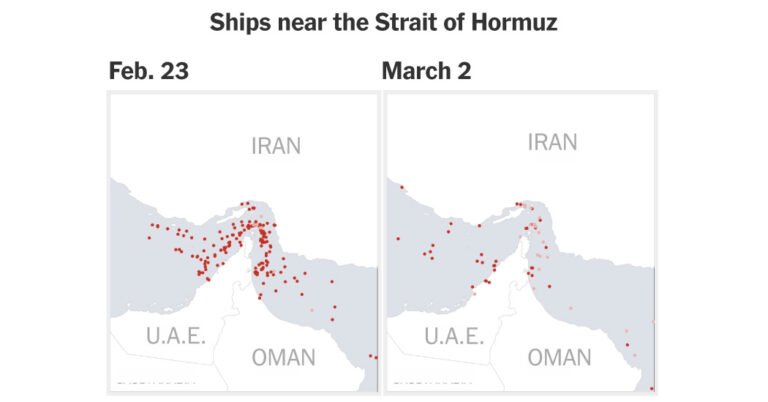

The US-Israel attack on Iran has pushed Bangladesh’s energy security to a critical juncture, with policymakers scrambling to assess the risks stemming from Tehran’s reported closure of the Strait of Hormuz – a key artery for global oil and gas trade.

If the conflict drags on, Bangladesh’s imports of liquefied natural gas, crude and finished products could face significant disruption, officials warn.

State-owned Bangladesh Oil, Gas and Mineral Corporation (Petrobangla) and Bangladesh Petroleum Corporation (BPC) have already sounded alarm bells over future fuel supplies.

Yesterday, the chiefs of Petrobangla and BPC briefed Power, Energy and Mineral Resources Minister Iqbal Hasan Mahmud Tuku on the current energy situation and possible courses of action.

Why Hormuz matters

The Strait of Hormuz is one of the world’s most critical shipping lanes, handling roughly 20% of global oil trade and about 20% of seaborne LNG shipments.

For Bangladesh – heavily dependent on imported fuels – this narrow maritime corridor is vital.

Petrobangla’s LNG import plan for March to May shows how exposed the country is. Over these three months, 22 LNG cargoes are scheduled to arrive in Bangladesh. Of them, 18 are supposed to pass through the Strait of Hormuz.

According to Petrobangla, six cargoes are expected in March, five in April, and seven in May, all to arrive via the Strait of Hormuz.

Petrobangla documents say the evolving Middle East situation has created uncertainty about supply through this sea route.

Speaking to TBS yesterday, Petrobangla Chairman Md Erfanul Haque said, “There is uncertainty, but no supplier has informed us of any disruption yet. If LNG supply under long-term contracts becomes strained, the spot market will be the only hope.”

A document presented to the energy minister echoed similar concerns, stating, “The five supplier companies must be emailed promptly to ascertain their stance on the LNG cargo supply. Additionally, the feasibility of importing LNG from the spot market needs to be confirmed urgently.”

Of the five suppliers, two are long-term and three are short-term contractors.

Long-term LNG supply under pressure

For March, seven cargoes are planned from QatarEnergy, QatarEnergy Trading and Oman Trading.

Of these, six are from Qatar – all transiting through the Strait of Hormuz – and one from Angola, Africa. Petrobangla said three of the six Qatari cargoes have already crossed the Strait.

For April, six cargoes are scheduled from QatarEnergy, QatarEnergy Trading, Oman Trading and Excelerate Energy. Five are from Qatar via Hormuz, and one from Angola.

And for May, nine cargoes are planned from QatarEnergy, QatarEnergy Trading, Oman Trading and Excelerate. Of them, seven are from Qatar via Hormuz, one from Angola and one from the United States.

Bangladesh plans to import a total of 115 LNG cargoes this year under long-term and short-term contracts and from the spot market. Of these, 103 will come under long- and short-term agreements, while 12 cargoes are expected from the spot market.

The Petrobangla chairman said the war came to a decisive stage following the killing of Iran’s leader, Ayatollah Khamenei. “I hope war will not drag on for a longer period of time. If it continues, we need to import LNG from the spot market.”

Officials warn that if the war prolongs, not only contracted supplies but also spot cargoes could be affected.

Refined fuel reserves: A mixed picture

While exposure to LNG imports through the Strait of Hormuz remains a concern, the BPC says refined fuel imports are relatively diversified in terms of sourcing, offering some cushion against immediate disruption.

According to BPC data, as of 27 February, the country’s current fuel reserves present a mixed scenario.

In terms of physical storage and usable stock, diesel has a total storage capacity of 6,24,189 tonnes, with 134,062 tonnes currently usable – equivalent to 10 days of consumption.

Octane has a storage capacity of 53,361 tonnes, with 33,640 tonnes available for use, providing a 28-day reserve.

Petrol storage capacity stands at 37,013 tonnes, of which 18,592 tonnes are usable, enough for 15 days.

Furnace oil has a storage capacity of 1,44,869 tonnes and a usable stock of 76,156 tonnes, ensuring supply for 93 days.

Jet fuel storage capacity is 64,118 tonnes, with 25,020 tonnes in usable stock, covering 13 days.

Kerosene has a storage capacity of 36,941 tonnes and 29,583 tonnes of usable stock, sufficient for 241 days.

Marine fuel storage capacity is 16,219 tonnes, with 4,675 tonnes available, enough to meet demand for 42 days.

Despite relatively low reserves for key products like diesel and petrol, BPC officials say there is no immediate cause for panic.

AKM Azadur Rahman, director (operations and planning) of BPC, said that long-term contracts from January to June legally bind suppliers to maintain shipments.

Refined products such as octane, petrol, furnace oil, jet fuel and kerosene are sourced from China, Malaysia, Indonesia, Australia and several Middle Eastern countries, reducing single-route dependency.

However, BPC officials caution that if crude supply chains linked to Hormuz are disrupted, downstream refined product availability could also face risks.

Rising oil price adds fiscal strain

Beyond supply risks, Bangladesh faces another challenge: surging global energy prices.

Following coordinated US and Israeli strikes on Iran on Saturday, Brent crude jumped by 10% to around $80 per barrel yesterday. Natural gas prices rose by 1.13%.

Markets are currently factoring in what analysts describe as a “war premium” – a risk-based price increase even without immediate physical supply losses.

Global market observers suggest if the conflict remains limited, prices could stabilise around $80 per barrel – compared to $62–$65 in February.

On the other hand, if shipping routes or oil infrastructure are disrupted, Brent could surpass $100 per barrel and in extreme scenarios, such as prolonged conflict or sustained closure of the Strait of Hormuz, prices could surge to $130–$140 per barrel.

For Bangladesh – already grappling with fiscal constraints and subsidy burdens – such a spike would be difficult to absorb.

Energy experts and policymakers say the country cannot afford both elevated oil prices and heavy reliance on expensive LNG from the spot market.

The Petrobangla chairman acknowledged the gravity of the situation.

“We are in a very tight situation. If LNG prices go out of reach, we will have no option but to cut supply.”

For now, no supplier has formally declared disruption. But officials admit the coming weeks will be crucial.

Bangladesh’s energy security, heavily intertwined with a narrow stretch of water thousands of miles away, now hinges on how the conflict in the Middle East unfolds.

No impact on fertiliser imports

The conflict in the Middle East is unlikely to disrupt Bangladesh’s fertiliser imports as there are currently no active procurement processes involving Middle Eastern countries, according to officials from the agriculture ministry and the Bangladesh Chemical Industries Corporation (BCIC).

The majority of imports for the current fiscal year have already been completed. Any remaining requirements will be met through sources outside the Middle East and the locally based Karnaphuli Fertiliser Company Limited (Kafco).

Official data at the agriculture ministry shows that as of 1 March, the country holds a stock of 16.85 lakh tonnes of fertiliser. This includes 4.99 lakh tonnes of urea stored by the BCIC. Additionally, the Bangladesh Agricultural Development Corporation (BADC), under the agriculture ministry, holds 3.53 lakh tonnes of MOP, 3.61 lakh tonnes of TSP, and 4.71 lakh tonnes of DAP.

Furthermore, 5.5 lakh tonnes will be procured from Kafco, located in Chattogram, while BCIC-affiliated factories will also continue their domestic production.

Fertiliser imports are managed by BADC and BCIC, with BCIC specifically responsible for urea imports.

Ahmed Faisal Imam, additional secretary (fertiliser management and inputs) at the agriculture ministry, believes that under the current circumstances, the country will face no fertiliser shortages until next November.

He told TBS that there is no concern regarding fertiliser supply for the Boro season, or even until next November. “The conflict between the US and Iran is not expected to have any immediate negative impact on Bangladesh’s fertiliser imports.”

He clarified that the final shipment of fertiliser purchased from Saudi Arabia was loaded onto vessels on 4 February and has already arrived in the country. Additionally, the vessels carrying fertiliser from Morocco are currently en route to Bangladesh. Notably, no ships currently carrying fertiliser for Bangladesh are required to pass through the Strait of Hormuz.

Md Moniruzzaman, director (commercial) of BCIC, and Md Saiful Alam, general manager (purchase) of BCIC, shared similar views.

However, a BCIC official, speaking on condition of anonymity, said that due to the ongoing gas crisis, domestic production might only reach a maximum of 7-8 lakh tonnes this year.

Bangladesh has an annual demand for various chemical fertilisers ranging from 58 lakh to over 68 lakh tonnes, more than 80% of which must be imported. The primary exporting nations include Saudi Arabia, Morocco, China, Qatar, Tunisia, the UAE, and Russia. Bangladesh maintains state-level agreements with Saudi Arabia, Qatar, and the UAE for these fertiliser imports.